How to Use the Tax Window Before It Closes

If you’re within 10 years of retirement, you have a powerful but time-sensitive opportunity sitting in your traditional IRA or 401(k): the ability to convert some of those pre-tax dollars to a Roth IRA and never pay taxes on them again.

A Roth conversion means paying taxes now on money you convert from traditional retirement accounts in exchange for tax-free growth and withdrawals forever. For pre-retirees, this can be one of the most impactful financial moves you make — but only if you do it right.

With 2026 tax rates now permanent and required minimum distributions starting at age 73, understanding when and how much to convert has never been more important.

How Roth Conversions Work

When you convert money from a traditional IRA or 401(k) to a Roth IRA, you’re essentially prepaying the taxes. You’ll owe income tax on the converted amount in the year you do it, but after that, the money grows tax-free and you can withdraw it tax-free in retirement.

Example:

Sarah converts $25,000 from her traditional IRA to a Roth in 2026.

She pays income tax on that $25,000 now — let’s say $6,000 in her 24% bracket.

But if that money grows to $50,000 over the next 10 years, she withdraws all $50,000 completely tax-free.

Compare that to leaving it in the traditional IRA, where she’d owe taxes on the entire $50,000 when she withdraws it — potentially at higher rates.

Why 2026 Is a Strategic Window

Several factors make 2026 particularly attractive for Roth conversions:

- Tax rates are now permanent. The current tax brackets are locked in, giving you predictable planning through retirement.

- The 10-year conversion runway. If you’re 55–65 now, you can spread conversions over multiple years before required minimum distributions kick in at age 73, keeping yourself in lower tax brackets each year.

- IRMAA planning opportunity. Converting now, while still working, can help reduce your future Modified Adjusted Gross Income and potentially avoid Medicare’s high-income surcharges later.

The New Jersey and Pennsylvania Advantage

Both New Jersey and Pennsylvania offer unique benefits for retirees that make Roth conversions even more attractive:

New Jersey: Retirement income from pensions, 401(k)s, and IRAs is generally tax- free for residents over 62 (with income limits). However, Roth conversions are taxed as regular income in the year you convert. The strategy: convert while you’re still working and paying NJ taxes anyway, then enjoy tax-free Roth withdrawals plus tax-free traditional retirement income later.

Pennsylvania: No state income tax on retirement income (pensions, traditional IRAs, 401(k)s, and Roth IRAs) at any age. Because Pennsylvania never allowed a deduction for traditional retirement contributions, Roth conversions are also completely tax-free at the state level. This makes Pennsylvania one of the strongest states for larger Roth conversions — you pay zero state tax on the conversion itself or on any future withdrawals.

When Roth Conversions Make the Most Sense

- You’re in a lower tax bracket now than you expect to be in retirement.

- You won’t need the converted money for at least 5 years.

- You want to leave tax-free money to your heirs — Roth IRAs have no required minimum distributions during your lifetime.

- You have cash outside of retirement accounts to pay the conversion taxes. Using retirement money to pay the tax bill defeats much of the purpose.

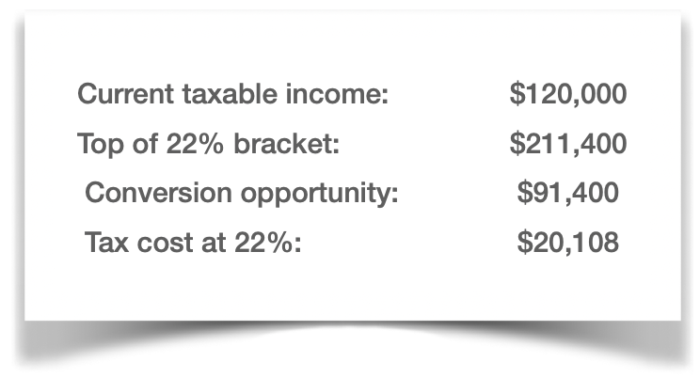

The Conversion Sweet Spot: How Much to Convert

The goal isn’t to convert everything — it’s to convert the right amount to optimize your lifetime tax bill.

The bracket-filling strategy: Convert just enough each year to fill up your current tax bracket without bumping into the next one (for married filing jointly).

Example calculation:

Every dollar converted within your current bracket costs less in taxes than it would in a higher bracket later.

Timing Your Conversions

December is decision time. You have until December 31 to complete conversions for the current tax year. This gives you most of the year to see how your income shapes up before committing.

Market downturns create opportunities. When your traditional IRA balance is temporarily lower, you can convert more shares for the same tax cost.

Retirement transition years are golden. The gap between when you stop working and when Social Security starts is often the lowest-income period of your adult life — perfect for larger conversions.

Common Mistakes to Avoid

- Converting too much at once — pushes you into higher brackets and can trigger Medicare surcharges.

- Ignoring the 5-year rule — each conversion starts its own 5-year clock. Convert money you won’t need for at least 5 years.

- Forgetting RMDs — once required minimum distributions start at age 73, they push up your income and limit conversion opportunities.

- Not coordinating with Social Security timing — large conversions can make more of your Social Security benefits taxable.

Frequently Asked Questions

Q: Can I undo a Roth conversion?

A: No. The ability to recharacterize conversions was eliminated in 2018. Once you convert, it’s permanent for that tax year.

Q: Do I have to convert my entire IRA?

A: Not at all. You can convert any amount you choose, from a few thousand dollars to the entire balance.

Q: What if I need the money before age 59½?

A: Converted principal can be withdrawn penalty-free after 5 years, regardless of age. Earnings follow regular Roth withdrawal rules.

Q: How do conversions affect my Medicare premiums?

A: Conversion income counts toward the Modified Adjusted Gross Income that determines Medicare Part B and Part D premiums. IRMAA surcharges kick in at $109,000 for individuals and $218,000 for couples in 2026.

Q: Should I convert if I live in a no-income-tax state?

A: Possibly. Even without state tax considerations, conversions can still make sense for federal tax planning and estate planning purposes.

Your Next Step

Roth conversion planning is highly personal — the right approach depends on your current tax bracket, retirement timeline, expected future income, and long-term estate goals.

If you’re within 10 years of retirement and hold substantial balances in traditional IRAs or 401(k)s, 2026 presents a powerful window of opportunity. At De Cesare Retirement Specialists, we specialize in running detailed Roth conversion projections that help pre-retirees in New Jersey and Pennsylvania minimize their lifetime tax burden and maximize tax-free retirement income.

Don’t let another year pass without exploring your options. Contact us today to schedule a complimentary, no-obligation Roth Conversion Strategy Session. Call 856-235-3830 or visit DeCesareRetirement.com to get started.

Click the image to download the guide in PDF

This report is provided for informational and educational purposes only and is not intended as tax, legal, or personalized investment advice. De Cesare Retirement Specialists and its principals are Certified Financial Planners™, not Certified Public Accountants. We do not provide tax preparation or tax advice. Any tax-related information is general in nature. You should consult with your own qualified tax professional or CPA before implementing any Roth conversion strategy, as individual results will vary based on your specific financial and tax situation.