A 2026 Income Planning Guide

The transition from earning a regular paycheck to creating retirement income represents one of the biggest financial shifts you’ll face. Unlike your working years when money arrived predictably every two weeks, retirement requires you to build a system that replaces that steady income flow.

This guide walks you through proven strategies to create a reliable retirement income that can replace your working paycheck. You’ll learn about withdrawal rates, income sources, and timing strategies that work for 2026 retirees.

Understanding Retirement Income Replacement

Your retirement income needs to cover the same expenses your paycheck handled during your working years. The key difference is that instead of one predictable source, you’ll likely draw from multiple income streams.

Most financial experts suggest replacing 70-90% of your pre-retirement income. However, your actual replacement needs depend on your specific situation. Some retirees need less because they no longer save for retirement or pay work-related expenses. Others need more due to healthcare costs or travel plans.

How Much Income Do You Really Need?

Start by calculating your current monthly expenses. Remove costs that disappear in retirement, like:

- Retirement plan contributions

- Work-related transportation

- Professional clothing and meals

- Payroll taxes on earned income

Add new retirement expenses such as:

- Increased healthcare premiums

- Long-term care insurance

- Travel and leisure activities

- Home maintenance (if you’re home more)

This gives you a clearer picture of your actual income replacement target.

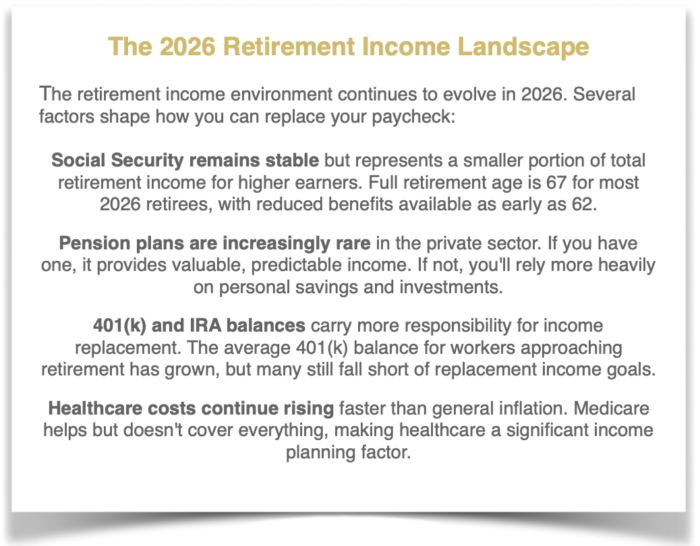

The 2026 Retirement Income Landscape

The retirement income environment continues to evolve in 2026. Several factors shape how you can replace your paycheck: