CFP® professional vs. Big Bank vs. Robo-Advisor

Whether you’re years from retirement or already there, choosing the right retirement planning advisor can make the difference between financial confidence and late-night worrying about money. But with so many options — CFP® professionals, big bank advisors, robo-advisors — how do you know which one fits your situation?

The truth is, not all financial advice is created equal. Some advisors are legally required to put your interests first, while others aren’t. Some charge transparent fees, while others earn commissions you might never see. Understanding these differences before you choose could save you thousands of dollars and help you retire with more confidence.

What is a CFP® professional?

A CFP® professional has earned one of the most rigorous certifications in financial planning. To earn the right to use those letters, they must complete extensive coursework, pass a comprehensive exam, gain professional experience, and commit to ongoing continuing education.

More importantly, CFP® professionals are held to a fiduciary standard and must act in your best interest when providing financial advice. This legal and ethical obligation places your interests first at all times during the advisory relationship.

What a CFP® professional typically does:![]()

- Creates comprehensive retirement income plans

- Coordinates Social Security timing with your other assets

- Helps with tax-efficient strategies including Roth conversions

- Plans for healthcare costs including Medicare decisions

- Works with you on estate planning basics

Best for: Pre-retirees and retirees who want personalized, holistic planning and have at least $250,000 in investable assets.

Big Bank Advisors: Convenient but Limited

If you bank with a large institution like Bank of America, Wells Fargo, or Chase, you’ve likely been invited to meet with their financial advisor. These advisors often have solid training and access to research, but there are important distinctions to understand.

The positives:

- Convenient if you already bank there

- Often no minimum account size to get started

- Access to a wide range of investment products

The challenges:

- Many follow a suitability standard rather than a fiduciary standard in all accounts.

- Some earn commissions on products, which can create conflicts of interest that must be disclosed.

- Advisor turnover can occur as staff changes

Best for: People just starting to save who want convenience and have straightforward financial situations.

Robo-Advisors: Efficient but Impersonal

Companies like Betterment, Wealthfront, and Vanguard Digital Advisor use algorithms to manage your investments. You answer questions online, they build a portfolio, and software handles the rebalancing.

The positives:

- Low fees — usually 0.25% to 0.50% per year

- No minimum investment required at most platforms

- Automatic rebalancing and tax-loss harvesting

The limitations:

- Many rely primarily on algorithms with limited human guidance for complex retirement decisions such as Social Security timing, Medicare, or estate coordination.

- The approach is generally standardized and may not fully address every unique personal situation. (Note: Some robo platforms now offer optional access to human advisors.)

Best for: Younger savers or people with straightforward situations who are comfortable managing most retirement decisions on their own.

How Much Should You Expect to Pay?

CFP® professionals: Typically charge 0.75% to 1.25% of assets under management annually. For someone with $500,000 invested, expect to pay $3,750 to $6,250 per year. Fees are negotiable and vary by client and the services provided. See Form ADV Part 2A for details.

Big bank advisors: May charge similar percentages, but watch for additional fees on mutual funds, trades, or account maintenance that can add up quickly.

Robo-advisors: Usually 0.25% to 0.50% annually. On $500,000, that is $1,250 to $2,500 per year.

The lowest fee is not always the best value when the advice is not tailored to your situation.

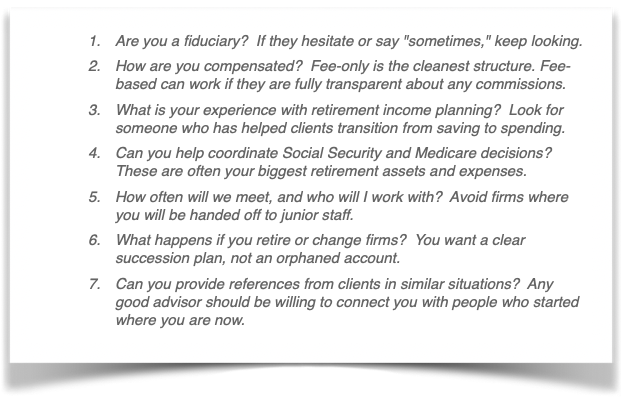

7 Questions to Ask Before You Hire Anyone

Red Flags to Watch For

- Promises of guaranteed returns or claims of consistently beating the market

- Pressure to move all your assets immediately

- Reluctance to explain fees clearly and in writing

- No written agreement outlining services and costs

- Urgency tactics like “you need to act now” on investment opportunities

A Simple Framework for Making Your Choice

Choose a CFP® professional if: You have $250,000 or more in assets, want comprehensive planning, and prefer working with the same advisor over time. Many clients find that the comprehensive planning provided by an independent CFP® professional can add value through tailored tax strategies, Social Security optimization, and proactive risk management—potentially offsetting the advisory fee. Actual results will vary based on each client’s situation.

Choose a big bank advisor if: You are just starting out, want convenience, and have a straightforward financial situation. Make sure you understand all fees upfront.

Choose a robo-advisor if: Your situation is straightforward, you are comfortable making most decisions yourself, and minimizing costs is your top priority.

Why Independence Matters for Retirement Planning

Independent advisory firms have one significant advantage: no institutional agenda. Unlike advisors at big banks or brokerage firms, independent CFP® professionals do not have sales quotas for proprietary products. They can recommend the best solution for you — whether that is a low-cost index fund, a CD, or simply holding more cash during uncertain times.

When your retirement security is at stake, that independence matters more than convenience. Although not every independent adviser is a CFP® professional, and not every CFP® professional is independent.

Your Next Step

The right retirement planning advisor should give you clarity and confidence about your financial future — not more confusion.

Ready to see if your current retirement plan is truly optimized?

Schedule a no-obligation, complimentary consultation with Steve De Cesare, CFP®. In this private meeting, we’ll review your Social Security timing, tax-efficient strategies (including Roth conversions), healthcare planning, and overall retirement income plan.

Call 856.235.3830, email info@DeCesareRetirement.com, or Click today.

This communication is for informational and educational purposes only and does not constitute personalized investment, tax, or legal advice. Investment advisory services are offered by De Cesare Retirement Specialists, a registered investment adviser. Registration does not imply a certain level of skill or training. There is no guarantee that any strategy discussed will be successful or achieve any particular outcome. Past performance is not indicative of future results. De Cesare Retirement Specialists is a registered investment adviser. Steve De Cesare, CFP®, is a CERTIFIED FINANCIAL PLANNER® professional and Investment Advisor Representative. The CFP® marks are owned by CFP Board in the U.S.