The Complete Guide

Planning for retirement raises one question above all others: how much money will I actually need? Most people either guess based on a generic rule of thumb or avoid the question entirely. Both approaches can cost you.

The truth is that retirement income planning is deeply personal. Two people with identical salaries can have retirement income needs that differ by hundreds of thousands of dollars. This guide gives you the framework, the math, and the real-world examples to calculate your specific number — not someone else’s.

Why Generic Rules of Thumb Fall Short

You have probably heard the 80% rule — plan to replace 80% of your pre-retirement income. It is a starting point, not a plan.

Research from the Employee Benefit Research Institute shows retirement spending varies dramatically among individuals. Some retirees spend 60% of their pre-retirement income. Others spend 120% or more. The difference comes down to healthcare, lifestyle, debt levels, family obligations, and where you live — none of which the 80% rule accounts for.

Step 1: Analyze Your Current Expenses Honestly

Start with 12 months of actual bank and credit card statements — not estimates. Most people discover they spend 15–25% more than they think they do.

Organize your spending into three buckets

Fixed expenses (continue regardless of employment):

- Housing — mortgage or rent, property taxes, insurance, maintenance

- Utilities — electricity, gas, water, internet, phone

- Insurance premiums — health, auto, life

- Minimum debt payments

Variable expenses (can be adjusted):

- Food and dining

- Transportation

- Entertainment and hobbies

- Clothing and personal care

- Travel and vacations

Periodic expenses (easy to forget, significant in total):

- Home maintenance and repairs

- Medical and dental costs

- Annual insurance payments

- Gifts and charitable giving

Add everything up. Multiply monthly totals by 12. That is your baseline annual spend.

Step 2: Project How Your Expenses Will Change in Retirement

Retirement does not simply reduce your expenses by 20%. Some costs drop. Others rise. Many stay exactly the same.

Expenses that typically decrease:

- Commuting, work clothing, work lunches — often $5,000–$10,000 per year

- Retirement savings contributions — money you were putting away stops

- Life insurance (if coverage is no longer needed)

- Mortgage payments (if paid off before retirement)

Expenses that typically increase:

- Healthcare — consistently the biggest surprise for retirees

- Travel and leisure — especially in the active early years of retirement

- Home maintenance — more time at home means more wear and awareness

- Hobbies and personal interests

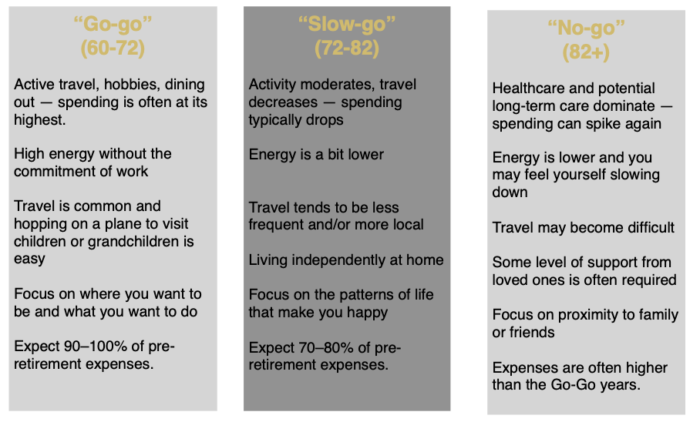

The three-phase reality of retirement spending

Most retirees move through three distinct phases:

Planning only for the middle phase is one of the most common and costly mistakes pre-retirees make.

Step 3: Calculate Your Income Replacement Ratio

Your replacement ratio is the percentage of your pre-retirement income you will need in retirement. This is more useful than a dollar amount alone because it scales with your income level.

How to calculate yours:

Take your projected annual retirement expenses (from Steps 1 and 2) and divide by your current gross annual income.

Example:

- Current gross income: $120,000

- Projected retirement expenses: $90,000

- Replacement ratio: 75%

Research from Investopedia shows that most people fall between 70% and 85%, but your personal ratio depends entirely on your lifestyle, debt, and health.

Higher earners tend to need lower ratios because a larger share of their income was going to savings and discretionary spending that disappears in retirement.

Lower earners tend to need higher ratios because most of their income was covering essential expenses that do not change.

Step 4: Account for Inflation — Especially Healthcare Inflation

Inflation is the silent tax on retirement income. At a 3% annual inflation rate, $60,000 today requires $80,635 in 10 years to buy the same things.

Use this formula to project your inflation-adjusted expenses:

Future Cost = Current Cost × (1 + inflation rate) ^ years until retirement

For general expenses, use 2.5–3%. For healthcare, use 5–6% — healthcare has consistently inflated faster than the rest of the economy.

Healthcare is its own line item. A healthy 65-year-old couple will spend an average of $345,000 for a couple (or $172,500 single) on healthcare throughout retirement, according to Fidelity’s 2025 estimates. These estimates exclude dental, vision, hearing aids, and over-the-counter (OTC) medications. That does not include long-term care.

Long-term care costs by setting*:

- Home health aide: $77,792–$80,080 per year (national average)

- Assisted living: $70,800–$74,400 per year

- Nursing home (private room): $127,750 per year

70% of people will need some form of long-term care, according to the U.S. Department of Health and Human Services. Plan for it.

Step 5: Calculate Your Income Gap

Now you have everything you need to find your actual gap.

Example: Mike and Linda, ages 62 and 60

- Combined current expenses: $95,000

- Retirement lifestyle adjustment (85%): $80,750

- Inflation adjustment (5 years at 3%): $93,670

- Healthcare buffer: $12,000

- Total annual retirement income needed: $105,670

Income sources:

- Social Security (both): $48,000

- Pension: $24,000

- 4% withdrawal from $850,000 in retirement accounts: $34,000

- Total income: $106,000

Mike and Linda have nearly covered their needs, with a small buffer for unexpected expenses.

Example: Sarah, age 55

- Current annual expenses: $68,000

- Retirement adjustment (80%): $54,400

- Inflation-adjusted (10 years): $72,896

- Healthcare buffer: $10,000

- Total needed: $82,896

Income sources:

- Social Security: $32,000

- 4% withdrawal from $340,000: $13,600

- Total: $45,600

Sarah’s gap: $37,296 per year . Additional savings needed: approximately $932,400

Sarah needs to significantly increase her savings or consider working a few additional years.

The 4% Rule: A Starting Point, Not a Guarantee

The 4% rule says you can withdraw 4% of your retirement portfolio in year one and adjust for inflation each year, and your money should last 30 years. It is a useful benchmark.

To use it: divide your annual income gap by 0.04 to find how much additional savings you need.

Example: $37,296 ÷ 0.04 = $932,400 in additional retirement assets needed.

Many planners now recommend 3–3.5% for people retiring before 65, given longer life expectancies and current market conditions.

Common Mistakes to Avoid

- Underestimating healthcare — Medicare does not cover dental, vision, hearing, or long-term care. Budget $5,000–$15,000 per year beyond premiums, depending on your health.

- Ignoring taxes — Traditional 401(k) and IRA withdrawals are taxable. If most of your savings are pre-tax, increase your income needs by 15–25% to cover taxes.

- Planning for average life expectancy — A healthy 65-year-old has a 50% chance of living past 85 and a 25% chance of reaching 92. Plan for 90–95.

- Using overly optimistic investment returns — Use 6–7% for planning purposes, not the historical 10% market average.

- Forgetting Social Security optimization — Claiming at 62 vs. 70 can mean a difference of $100,000+ in lifetime benefits.

Working With a Certified Financial Planner® Professional

You can do basic retirement income calculations yourself. But if you have multiple income sources, significant assets, or complex tax situations, working with a CFP professional pays for itself.

A Certified Financial Planner® professional uses sophisticated planning software to model multiple scenarios — market downturns, inflation spikes, long-term care events — and helps you stress-test your plan before you need to rely on it.

![]()

At De Cesare Retirement Specialists, we work exclusively with pre-retirees and retirees navigating exactly these decisions. Our CFP® professional brings 26 years in the investment industry and 14 years of Five Star Wealth Manager recognition to every client relationship — not a call center, not a robo-advisor, not a junior associate. One advisor, your plan.

Frequently Asked Questions

How much money do I need for retirement? Most people need 70–90% of their pre-retirement income, but your personal number depends on your specific expenses, health, and retirement lifestyle. Use the 5-step process in this guide to calculate your actual target.

What is the 4% rule? The 4% rule suggests withdrawing 4% of your portfolio in year one and adjusting for inflation annually. At this rate, your money has historically lasted 30+ years. For early retirement or conservative planning, use 3–3.5%.

How do I estimate my Social Security benefits? Visit ssa.gov and create a My Social Security account. You will see personalized benefit estimates at different claiming ages based on your actual earnings history.

Should I include my home equity in retirement calculations? Your primary residence can contribute through downsizing, a reverse mortgage, or rental income — but do not count the full value since you need somewhere to live. Count only the equity above your future housing costs.

How much should I budget for healthcare? Plan for healthcare to represent 15–20% of your retirement income. A healthy couple should budget approximately $345,000 for a couple (or $172,500 single), excluding dental, vision, hearing aids, and OTC medications, not including long-term care costs.

When should I start calculating my retirement income needs? As early as possible — ideally in your 40s. But it is never too late. Even if you are 5 years from retirement, a clear income target helps you make the right decisions about timing, lifestyle, and savings rate.

What if I cannot save enough? Options include working a few additional years, reducing planned retirement expenses, relocating to a lower-cost area, pursuing part-time work in early retirement, or optimizing Social Security timing. A CFP professional can help you evaluate which combination makes the most sense.

You spent decades earning this money. Take the time to understand exactly how much retirement requires — and build a plan that makes it last.

Ready to calculate your true retirement income needs with a CFP® professional? Contact De Cesare Retirement Specialists at 856.235.3830 or email info@DeCesareRetirement.com today for a no-obligation conversation.

https://www.nasdaq.com/press-release/carescout-releases-2025-cost-care-survey-results-2026-03-02 https://aspe.hhs.gov/reports/what-lifetime-risk-needing-receiving-long-term-services-supports-0 https://newsroom.fidelity.com/pressreleases/fidelity-investments–releases-2025-retiree-health-care-cost-estimate–a-timely-reminder-for-all-gen/s/3c62e988-12e2-4dc8-afb4-f44b06c6d52e *Figures are national medians/averages as of the most recent available data and will vary significantly by location, health status, and longevity. Actual costs in New Jersey are typically higher. Fidelity/CareScout figures as of 2025; costs rise annually. This communication is for informational and educational purposes only and does not constitute personalized investment, tax, or legal advice. Investment advisory services are offered by De Cesare Retirement Specialists, a registered investment adviser. Registration does not imply a certain level of skill or training. There is no guarantee that any strategy discussed will be successful or achieve any particular outcome. Past performance is not indicative of future results. De Cesare Retirement Specialists is a registered investment adviser. Steve De Cesare, CFP®, is a CERTIFIED FINANCIAL PLANNER® professional and Investment Advisor Representative. The CFP® marks are owned by the CFP Board in the U.S.